TL;DR

- S&P 500 rose 3.18%, and Nasdaq rose 4.14% for the holiday-shortened week on hopes of de-escalation in Iran and Powell’s dovish signal. Yet Q1 2026 remains the worst quarter in four, with the S&P 500 down 4.6% YTD.

- March Nonfarm Payroll increased by 178K, with unemployment falling to 4.3%. Labor market resilience complicates the Fed’s rate-cut calculus even as geopolitical uncertainty clouds the outlook.

- WTI crude increased by 11.41% on the week, a total of 93% increase YTD, as Oman mediates a monitoring protocol. Without a clear resolution timeline, the risk of energy inflation is elevated.

- Crypto markets rebounded last week, with BTC up 4.6% and ETH up 6.4%, although sentiment remained firmly in Extreme Fear at 11.

- Memecore stood out as the top outperformer with 20.3% gain after its latest hard fork boosted sentiment around lower fees and faster transactions.

- Circle enters wrapped Bitcoin market with cirBTC as institutional BTC infrastructure race heats up.

- Big Tech backs x402 Foundation as push for agentic AI payment rails gains institutional support.

- Better Money raises $10M to build stablecoin clearinghouse as fragmentation across issuers and chains becomes a scaling bottleneck.

Macro Overview

Strong Payrolls Ease Recession Fears while U.S. Equities Post Best Weekly Gain of 2026, Causing “Higher-for-Longer” Probability to Persist

US equity markets had a powerful recovery during the holiday-shortened week, snapping the five-week losing streak. S&P 500 surged 3.18% for the week, the Dow Jones Industrial Average gained 2.85%, and the Nasdaq Composite outperformed with a 4.14% advance, driven by strength in large-cap technology names. The rebound was fueled by 3 factors: easing Treasury yields, quarter-end and month-end rebalancing flows, and growing optimism about a potential de-escalation in the US–Iran conflict. The US signaled willingness to end hostilities if the Strait of Hormuz is reopened, combined with Iran indicating readiness to end the war, sparked a two-day relief rally mid-week. Despite the weekly gain, the S&P 500 ended Q1 2026 down 4.6%, the Nasdaq fell 7.1% YTD, and the Dow dropped 3.6% for the quarter, the first quarterly loss in four quarters. March alone saw the S&P 500 lose 5.1%, its worst monthly performance since 2022, underscoring the cumulative damage from geopolitical and energy-driven headwinds.

The March employment report delivered a significant upside surprise, with nonfarm payrolls increasing by 178,000 and far exceeding the consensus forecast of 59,000–70,000, reversing February’s revised loss of 133,000 jobs. Private payrolls grew by 186,000, well above the 70,000 expected. The unemployment rate dipped to 4.3% from 4.4%, though the decline partly reflected people dropping out of the labor force rather than net new employment. The rebound was attributed to the end of a healthcare sector strike and the abatement of harsh winter weather that had suppressed February’s figures. The unexpectedly robust labor data present a strategic paradox for the Federal Reserve. While current employment figures suggest systemic resilience, they fail to account for the subsequent economic disruptions triggered by the US-Iran War. This retrospective strength diminished the immediate justification for monetary easing, causing initial market optimism to fade as investors recalibrated for a “higher-for-longer” environment shadowed by escalating geopolitical volatility.

Federal Reserve Chair Jerome Powell delivered a notably reassuring message last week, stating that the Fed is inclined to “look through” the short-term oil price surge, treating it as a transitory supply shock rather than a persistent inflation driver. He acknowledged that “patience has limits” if oil-driven inflation becomes entrenched, but emphasized the Fed’s data-dependent approach. The FOMC meeting minutes from March 18 are scheduled for release next week and will provide additional insight into the committee’s deliberations. Major Wall Street brokerages, including Morgan Stanley, maintained forecasts for two rate cuts in 2026, targeting a terminal rate of 3.00–3.25%.

Next week’s calendar is dominated by inflation data that will directly test Powell’s ‘look-through’ thesis. Friday’s March CPI is the critical release: consensus expects +0.9% MoM and +3.4% YoY, the highest annual rate since April 2024, driven by the surge in oil prices. A hotter-than-expected print could force markets to reprice Fed policy more hawkishly. Thursday’s February Core PCE will be stale but provides a baseline for the Fed’s preferred gauge. Geopolitically, the Iran-Oman mediation protocol remains the key variable. Any concrete progress toward reopening the Strait of Hormuz would trigger a sharp decline in oil prices and a risk-asset rally, while a breakdown could push Brent back toward $120+. Overall, markets face a high-stakes week where inflation data and geopolitical headlines will compete for dominance. (1)

DXY

The DXY rose to 100.185, driven by a “safe-haven” bid and robust labor data. While geopolitical tensions eased mid-week, the blockbuster 178,000 NFP print forced markets to price in a “higher-for-longer” Fed stance. This divergence between resilient U.S. growth and global instability continues to underpin greenback strength. (2)

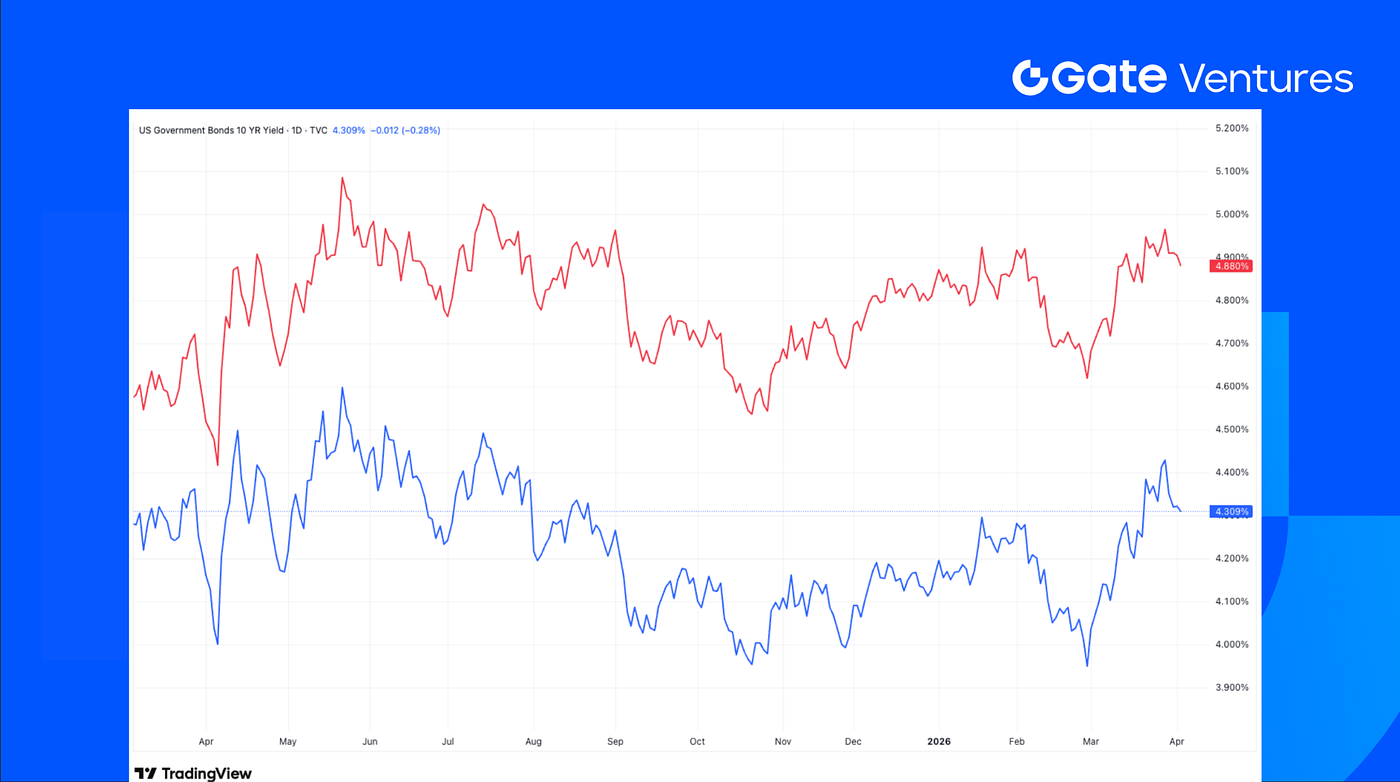

US 10-Year and 30-Year Bond Yields

Yields trended lower despite strong employment, as Powell’s “look through” stance on oil shocks reassured bondholders. The decline reflects quarter-end rebalancing flows and technical buying after the recent sell-off. Investors are currently prioritizing the potential de-escalation of the US-Iran conflict over the lagging, pre-war strength shown in March payrolls. (3)

Gold

Gold surged past 4,670, hitting new highs as a hedge against the risks of Middle East warfare and new trade tariffs. Despite a stronger dollar, gold’s ascent underscores deep-seated fears that inflation may become entrenched if the Strait of Hormuz remains contested, maintaining a historic geopolitical risk premium. (4)

Crypto Markets Overview

1. Main Assets

BTC Price

ETH Price

ETH/BTC Ratio

BTC rose 4.6% last week, while ETH outperformed with a 6.4% gain. Spot BTC ETFs recorded net inflows of $22.3M, whereas spot ETH ETFs saw net outflows of $42.2M. (5)

The ETH/BTC ratio increased 1.7% over the week, while overall market sentiment remained deep in Extreme Fear at 11. (6)

2. Total Market Cap

Crypto Total Marketcap

Crypto Total Marketcap Excluding BTC and ETH

Crypto Total Marketcap Excluding Top 10 Dominance

Total crypto market cap rose 3.5% last week, while market cap excluding BTC and ETH increased 0.4%. Market cap excluding the top 10 tokens by dominance also gained 1.5%, pointing to a more modest rebound across the broader altcoin market.

Source: Coinmarketcap and Gate Ventures, as of 7th Apr 2026

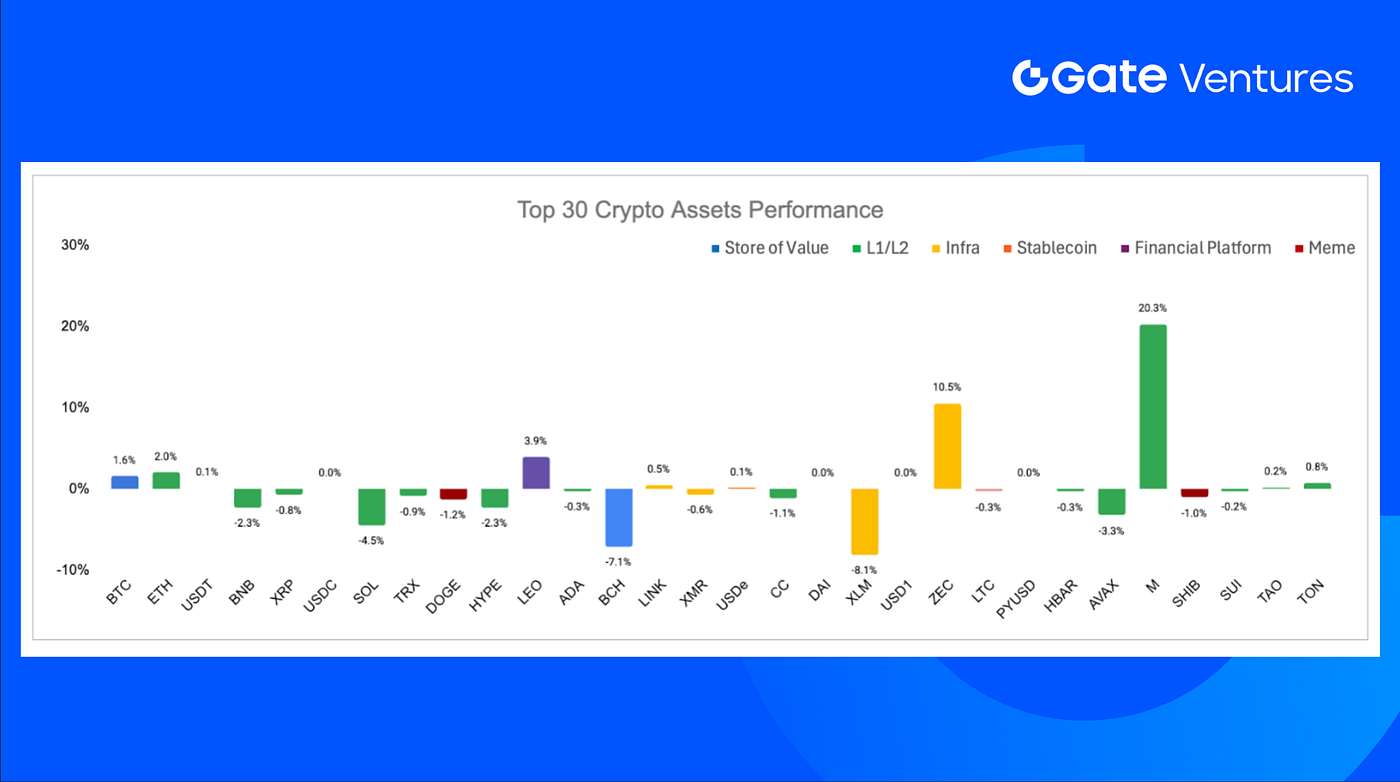

Among the top 30 assets, prices declined ~0.1% on average, Memecore, Zcash, and LEO led the gain.

Memecore led the market with a 20.3% gain, driven by positive momentum following its latest hard fork. The upgrade, which introduced lower gas fees and faster transaction speeds, appears to be having an immediate impact on market sentiment. (7)

The Key Crypto Highlights

China’s State Administration of Taxation and the National Financial Regulatory Administration have jointly urged banks and local authorities to integrate blockchain and privacy-computing technologies into the “bank-tax interaction” framework to improve credit access for small and medium-sized enterprises. The policy directive emphasizes standardized tax-data sharing between regulators, financial institutions and businesses to reduce information asymmetry, enhance credit-approval efficiency and expand financing supply to compliant taxpayers. The initiative aligns with China’s broader national data-infrastructure strategy, following a 2025 roadmap targeting nationwide blockchain deployment by 2029 and an estimated 400 billion yuan ($58 billion) in annual investment into blockchain-based data systems. (8)

2. Circle enters wrapped Bitcoin market with cirBTC as institutional BTC infrastructure race heats up

Circle is expanding beyond stablecoins into Bitcoin infrastructure with the launch of cirBTC, a 1:1 Bitcoin-backed wrapped asset designed for institutional users including OTC desks, market makers and lending protocols. The product will debut on Ethereum and also be available through Circle’s Arc network and Circle Mint, positioning the company to compete directly with BitGo’s WBTC and Coinbase’s cbBTC as institutions look for more secure and neutral ways to deploy Bitcoin in DeFi. (9)

3. Big Tech backs x402 Foundation as push for agentic AI payment rails gains institutional support

Google, Microsoft and Amazon Web Services are among the major firms backing the newly launched x402 Foundation, which was set up under the Linux Foundation to govern and standardize the x402 protocol for AI-native payments across crypto and fiat rails. The move gives x402 a neutral, open-source home and signals growing industry support for agentic payments as AI agents increasingly transact online for APIs, data and digital services, even as recent onchain activity for the protocol has cooled sharply from its late-2025 peak. (10)

Key Ventures Deals

1. The Better Money raises $10M to build stablecoin clearinghouse as fragmentation across issuers and chains becomes a scaling bottleneck

The Better Money has raised $10 million in funding led by a16z crypto to build a stablecoin clearinghouse designed to unify fragmented stablecoin liquidity across issuers, chains and payment platforms. The infrastructure aims to allow builders and issuers to integrate once and transact supported stablecoins at par across networks, positioning the clearinghouse as a coordination layer similar to legacy fiat settlement rails such as ACH and Fedwire. The move highlights growing industry focus on interoperability infrastructure as stablecoins scale toward becoming a global payment layer. (11)

2. Pixie Chess raises $5.2M seed as onchain game studios continue experimenting with crypto-native game design

Pixie Chess, a Web3 game blending elements of chess, trading card games and NounsDAO-inspired crypto culture, has raised a $5.2 million seed round led by Paradigm, with additional backing from Seed Club and a group of angel investors. Incubated through the Paradigm EIR program. (12)

3. Kulipa raises $6.2M seed as stablecoin card issuance infrastructure gains traction with fintechs and wallets

Kulipa, a stablecoin card issuing infrastructure platform, has raised a $6.2 million seed round co-led by Flourish Ventures and 1kx to expand its white-label card issuance services, with a particular focus on entering the US market. The company helps fintechs and crypto wallets launch stablecoin payment cards without directly managing processing, fraud, prefunding or settlement, positioning itself as a middleware layer that lowers the operational barriers to stablecoin-linked consumer spending. The raise highlights growing demand for infrastructure that can connect stablecoin balances to everyday card payments through more compliant and scalable enterprise distribution. (13)

Ventures Market Metrics

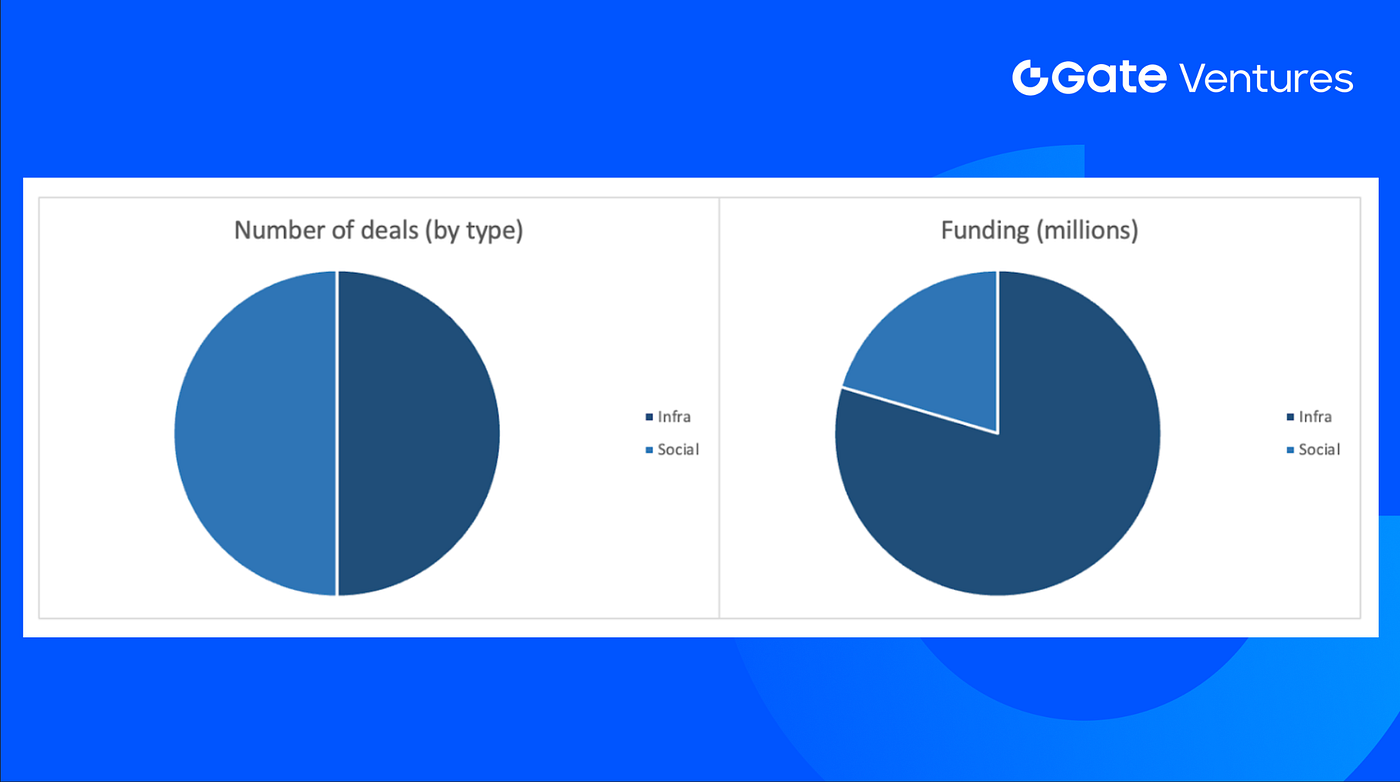

The number of deals closed in the previous week was 6, with Infra and Social having 3 deals respectively.

Weekly Venture Deal Summary, Source: Cryptorank and Gate Ventures, as of 7th Apr 2026

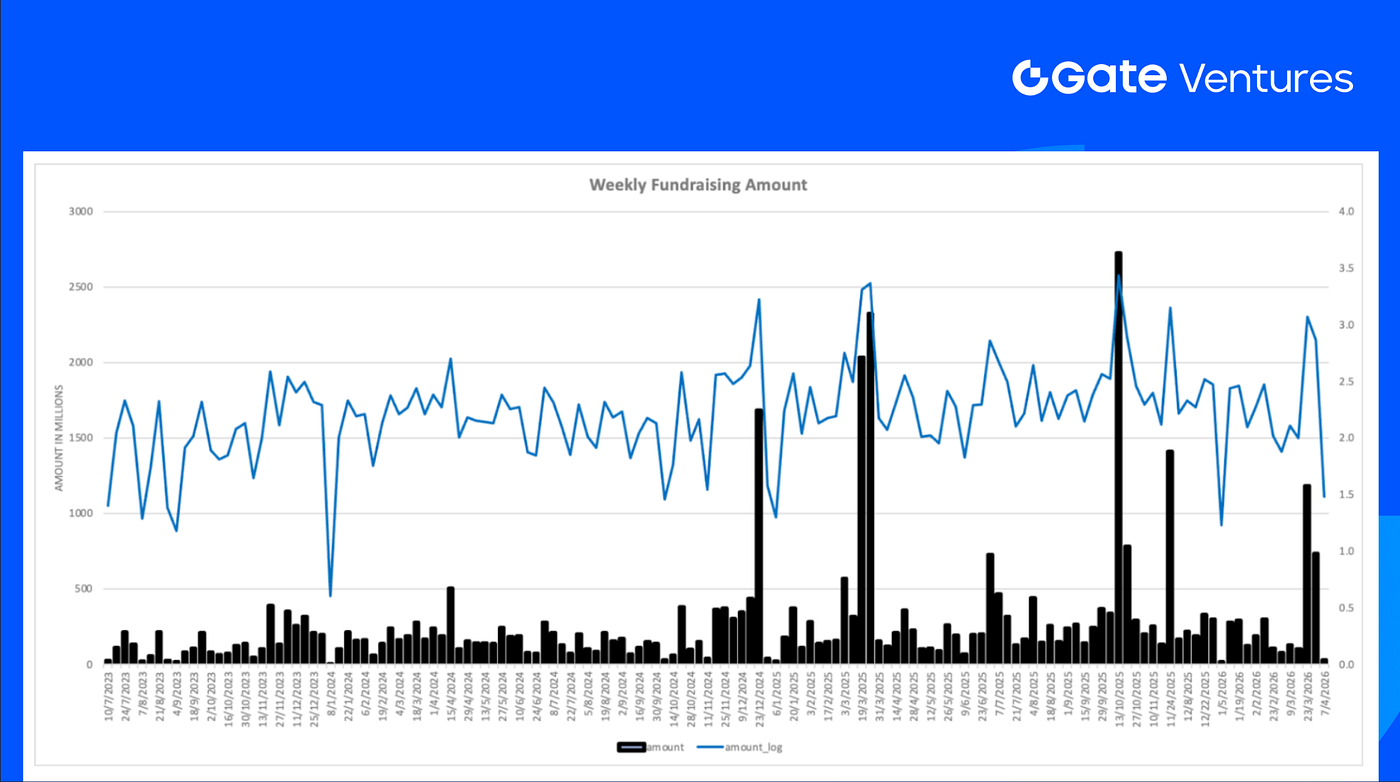

The total amount of disclosed funding raised in the previous week was $30.4M, 1 deal in the previous week didn’t announce the raised amount. The top funding came from the Infra sector with $24.2M. Most funded deals: The Better Money ($10M).

Weekly Venture Deal Summary, Source: Cryptorank and Gate Ventures, as of 7th Apr 2026

Total weekly fundraising declined to $30.4M for the first week of Apr-2026, a decrease of 96% compared to the week prior.

About Gate Ventures

Gate Ventures, the venture capital arm of Gate.com, is focused on investments in decentralized infrastructure, middleware, and applications that will reshape the world in the Web 3.0 age. Working with industry leaders across the globe, Gate Ventures helps promising teams and startups that possess the ideas and capabilities needed to redefine social and financial interactions.

Website | Twitter | Medium | LinkedIn

The content herein does not constitute any offer, solicitation, or recommendation*.* You should always seek independent professional advice before making any investment decisions. Please note that Gate Ventures may restrict or prohibit the use of all or a portion of the services from restricted locations. For more information, please read its applicable user agreement.

Reference:

- Trading Economic Ahead Economic Preview, https://www.spglobal.com/market-intelligence/en/news-insights/research/2026/04/week-ahead-economic-preview-week-of-6-april-2026

- DXY Index, TradingView, https://www.tradingview.com/chart/z1UD772v/?symbol=TVC%3ADXY

- US 10 Year Bond Yield, TradingView, https://www.tradingview.com/chart/B9cgEklh/?symbol=TVC%3AUS10Y

- Gold Price, TradingView, https://www.tradingview.com/chart/z1UD772v/?symbol=TVC%3AGOLD

- BTC & ETH ETF Inflow, https://sosovalue.com/tc/assets/etf/us-btc-spot

- BTC Greed and Fear Index, https://alternative.me/crypto/fear-and-greed-index/

- Memecore hardfork, https://advertorial.cryptonews.com/press-releases/memecore-hard-fork-lifts-m-above-260-as-risk-off-markets-push-attention-toward-presales-like-maxi-doge/

- China’s regulators push banks to adopt blockchain-based lending infrastructure as data-sharing reform accelerates, https://cointelegraph.com/news/china-tax-authority-banks-implement-blockchain-lending

- Circle enters wrapped Bitcoin market with cirBTC as institutional BTC infrastructure race heats up, https://cointelegraph.com/news/circle-launch-cirbtc-wrapped-bitcoin-token-targeting-institutional-markets

- Big Tech backs x402 Foundation as push for agentic AI payment rails gains institutional support, https://cointelegraph.com/news/big-tech-companies-join-x402-protocol-agentic-ai

- Better Money raises $10M to build stablecoin clearinghouse as fragmentation across issuers and chains becomes a scaling bottleneck, https://x.com/SamBroner/status/2038971745713918234

- Pixie Chess raises $5.2M seed as onchain game studios continue experimenting with crypto-native game design, https://x.com/joshqharris/status/2039740009444438520

- Kulipa raises $6.2M seed as stablecoin card issuance infrastructure gains traction with fintechs and wallets, https://www.theblock.co/post/396063/stablecoin-card-kulipa-seed-round?utm_source=twitter&utm_medium=social