MicroStrategy purchased $264.1 million worth of BTC from January 20-25 by issuing stock financing. mNAV has fallen to 0.94, a 6% discount, with only a 0.38% increase in BTC per share. Dilution rate is 5.36%, catching up with the cumulative rate of 5.77%, and issuing at a discount damages shareholder value.

mNAV Breaks Below 1.0, Dilution Effect Consumes Value

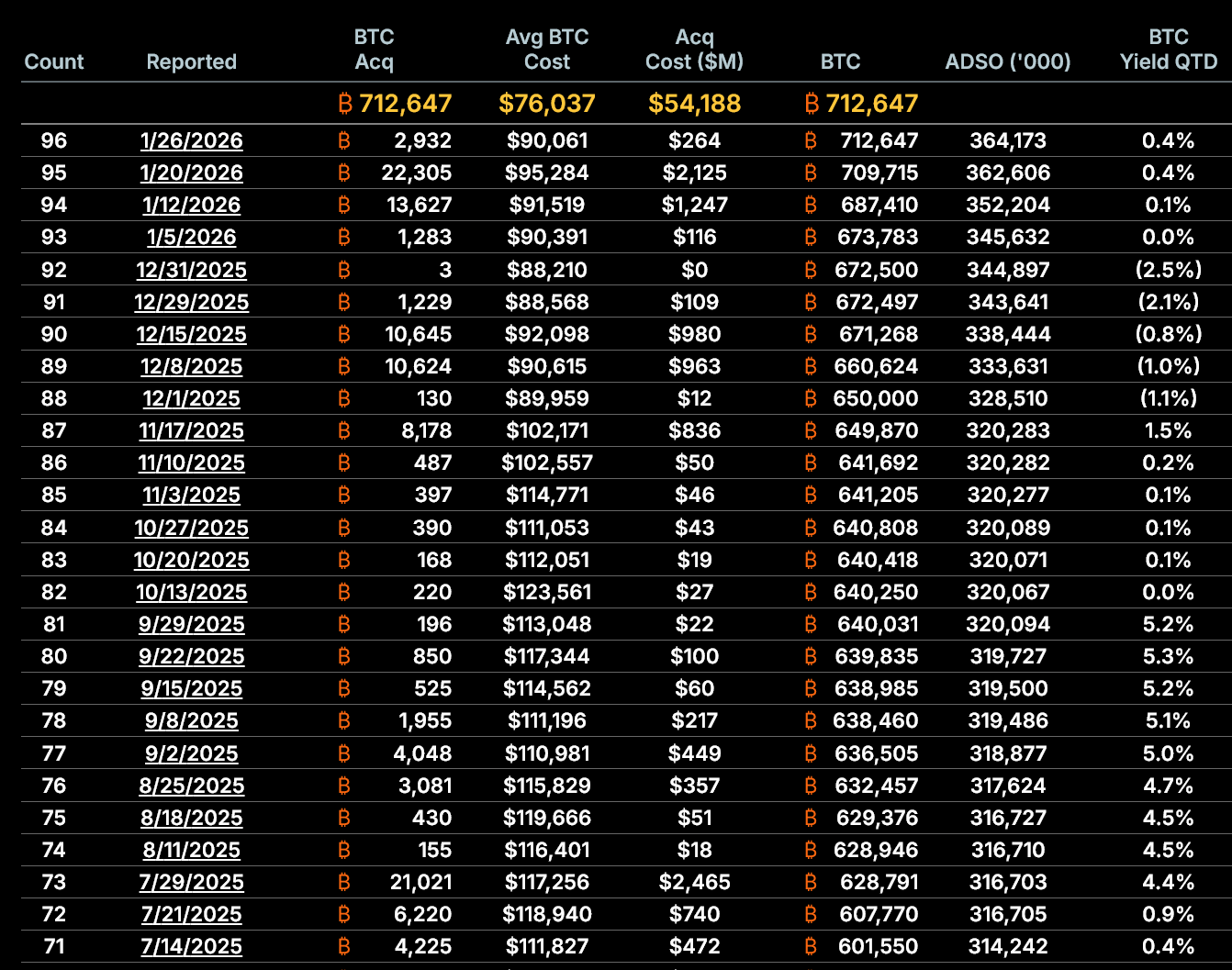

(Source: SaylorTracker)

The most important structural indicator for MicroStrategy is its net asset value multiple (mNAV), which measures the trading of its stock relative to the value of Bitcoin held per share. As of January 26, MicroStrategy’s post-dilution mNAV is approximately 0.94, meaning the stock trades at a 6% discount to the Bitcoin backing per share. This is critical because MicroStrategy’s strategy relies on issuing stock at a price above net asset value. When shares trade at a discount, new issuance not only fails to create shareholder value but actually erodes it.

This mechanism can be explained with simple math. Suppose each share of MicroStrategy corresponds to 0.002 BTC, with BTC priced at $90,000, giving an intrinsic value of $180 per share. If the stock trades at $200 (mNAV = 1.11), issuing new shares to raise $200 can buy 2.22 USD worth of BTC (200/90,000 = 0.00222 BTC). The BTC per share increases from 0.002 to slightly above 0.002, benefiting shareholders. But if the stock trades at $170 (mNAV = 0.94), issuing new shares to raise $170 can only buy 0.00189 BTC, which dilutes the original shareholders’ BTC holdings.

Historically, MicroStrategy has justified issuing stock by increasing the per-share Bitcoin value. But this growth effect is now waning. According to company data, as of January 5, MicroStrategy held 673,783 BTC, equivalent to 345.6 million diluted shares, or 0.001949 BTC per share. By January 26, holdings increased to 712,647 BTC, but diluted shares rose to 364.2 million, with each share valued at 0.001957 BTC. That’s only a 0.38% increase from the previous month.

More importantly, from January 20 to January 26, the BTC per share remained nearly unchanged. This indicates that recent stock issuances no longer meaningfully increase the proportion of Bitcoin held by shareholders. Bitcoin price growth can no longer offset the increasing dilution effect.

Dilution Rate Accelerates to Catch Up with Cumulative Growth

(Source: SaylorTracker)

The dilution rate is accelerating. From January 5 to January 26: the number of diluted shares increased by 5.36%, while Bitcoin holdings increased by 5.77%. Although the total holdings remain slightly above the dilution amount, the gap has narrowed sharply in the past week. This widening gap coincides with the decline in mNAV, indicating the model’s efficiency is decreasing. If the stock price continues below net asset value, further issuance mathematically reduces the Bitcoin exposure per share.

If this trend persists, it will fundamentally change MicroStrategy’s investment logic. Investors buy MicroStrategy stock mainly for leverage and appreciation potential that surpasses direct Bitcoin ownership. If the BTC per share stops growing or even declines, MicroStrategy loses its advantage over direct BTC holdings. Investors may then prefer to buy BTC directly or via BTC ETFs, avoiding company risk and stock volatility.

This Bitcoin strategy still relies entirely on capital market access. Over the past 19 months, the company has raised approximately $18.56 billion through common stock issuance, issuing about 22.66 million shares. This latest acquisition continues that trend, further diluting equity amid a weak market. The company is increasingly relying on preferred stock, which grants shareholders priority over common stockholders with fixed claims. While issuing preferred stock can sustain Bitcoin purchases during market downturns, it also increases long-term debt and complicates the balance sheet.

Preferred Stock Increases Structural Risk

(Source: MicroStrategy)

MicroStrategy’s multi-layer preferred stock products such as STRC, STRK, STRF, STRD offer high dividends of 8-11%, attracting income-focused investors. These preferred stock issuances provide an alternative financing channel when stock prices are weak. However, preferred stocks are inherently debt-like financing instruments requiring regular dividend payments. MicroStrategy does not pay these dividends from operational profits but continues to issue new securities to fund them, creating a cycle dependency.

This cyclical financing works in a rising market but faces huge risks in a declining market. If BTC prices remain low, MicroStrategy’s stock could fall further, increasing the discount on mNAV, and making new share issuance more dilutive. Meanwhile, to pay preferred dividends, the company must keep issuing securities, further exacerbating dilution. Once this vicious cycle starts, it could lead to a spiral decline in shareholder value.

The recent issue with MicroStrategy’s Bitcoin purchases is not about scale or timing but about its structure. With mNAV below 1.0, the appreciation of Bitcoin per share is near zero, equity dilution accelerates, dependence on capital markets deepens, and the company’s core strategy faces unprecedented challenges. Unless the stock premium returns, continuous accumulation of Bitcoin may shift from appreciation to dilution. Even if Bitcoin prices rebound, this shift will fundamentally alter shareholder risk profiles.

Current data shows MicroStrategy can still buy Bitcoin, but the question is whether it can continue doing so without damaging shareholder value. The increasingly likely answer is no.

Disclaimer: The information on this page may come from third parties and does not represent the views or opinions of Gate. The content displayed on this page is for reference only and does not constitute any financial, investment, or legal advice. Gate does not guarantee the accuracy or completeness of the information and shall not be liable for any losses arising from the use of this information. Virtual asset investments carry high risks and are subject to significant price volatility. You may lose all of your invested principal. Please fully understand the relevant risks and make prudent decisions based on your own financial situation and risk tolerance. For details, please refer to

Disclaimer.

Related Articles

The New York Times reignites the “Satoshi identity mystery”; after Adam Back was targeted, he quickly clarified

Author: Nancy, PANews

Satoshi Nakamoto’s real identity remains the mystery that has continued for 17 years in the crypto world. Guesses surrounding this pseudonym have never stopped—candidates ranging from cryptographers to company founders have come and gone, yet there has always been a lack of decisive evidence.

Recently, The New York Times published a 10,000-plus-word investigation. Based on multiple comparisons drawn from language style, technical paths, and historical context, it ranked Blockstream CEO Adam Back as the strongest candidate for Satoshi Nakamoto. However, this claim was quickly and explicitly denied by Back himself, and the relevant arguments were widely questioned by the industry as difficult to substantiate.

Satoshi Nakamoto identity controversy flares up again; the 10,000-plus-word investigation targets Adam Back

In this investigation, New York Times reporter John Carreyrou spent more than a year deeply sorting through decades of archives and the cypherpunk email mailing lists to

区块客4m ago

Morgan Stanley Bitcoin ETF Drives 3-Fold Impact as 16,000 Advisors Open Path to Multi-Billion Demand

Bitcoin demand is set to expand rapidly as Morgan Stanley deploys its 16,000 advisors and launches a low-cost ETF, driving institutional inflows and strengthening crypto’s position in mainstream portfolios.

Key Takeaways:

Morgan Stanley’s 16,000 advisors unlock major bitcoin demand, driving

Coinpedia4h ago

DWF Labs Co-Founder: The current market is boring, but it hasn’t disappeared—builders or investors still have a lot to do.

DWF Labs co-founder Andrei Grachev said the market is currently in a “boring” phase, with many important activities quietly underway. He advised investors to stay patient and look for a better timing. He emphasized that opportunities still exist in the market—such as holding Bitcoin or participating in altcoins—and urged retail investors to keep learning and remain optimistic.

GateNews5h ago

Researchers propose a transaction scheme for quantum-resistant Bitcoin without needing a fork

Gate News message, on April 12, a researcher proposed a transaction scheme that enables quantum-resilient protection for Bitcoin without requiring a fork. At present, the quantum computing threat to Bitcoin is still at the theoretical level. Meanwhile, tech companies such as Google and Cloudflare have already begun preparing countermeasures and set a target timeline to complete the migration of quantum cryptography after 2029.

GateNews5h ago

Contract whale “sets 10 big targets first” — the short position is up $3.21 million; the BTC short opening price is $71,554.61.

Gate News message, April 12, according to on-chain analyst Ai Yi (@ai_9684xtpa) statistics, the short positions of the contract whale “first set 10 big targets” (@Jason60704294) are currently up $3.21 million. Of this, the BTC short positions are 2,567.49 BTC, with an opening price of $71,554.61, and an unrealized profit of $1.19M; the ETH short positions are 38,465.22 ETH, with an opening price of $2,248.74, and an unrealized profit of $2.03M.

GateNews5h ago